The Case for Thinking in Bitcoin per Share

The metric that measures whether Strategy is increasing each share’s proportional ownership of bitcoin.

Before I Understood Strategy’s Bitcoin per Share, I Understood My Own

Before I understood Strategy’s bitcoin per share, I understood my own. At some point after buying MSTR and GBTC in my Roth IRA in 2020, I stopped asking how many dollars my account was worth. Instead, I started asking a different question: how much bitcoin did my account effectively represent?

When I bought my first MSTR shares, in my Roth IRA I owned some GBTC and some other non-bitcoin stocks. By the end of 2020, I only had MSTR and GBTC in my Roth IRA, held 50/50 in USD terms.

Somewhere after that I started to think about what I owned with MSTR. When I first bought it, I saw a company with no debt and earning free cash flow of about $100 million per year but with no growth prospects. After Strategy took the cash on its balance sheet and bought bitcoin, I effectively had proportional ownership of the bitcoin on its balance sheet (though that ownership was non-redeemable).

As for GBTC, I also effectively had proportional ownership of the underlying bitcoin (though that ownership was also non-redeemable). With GBTC, I also had to pay a fee, which was effectively eating away at the amount of bitcoin represented by each share.

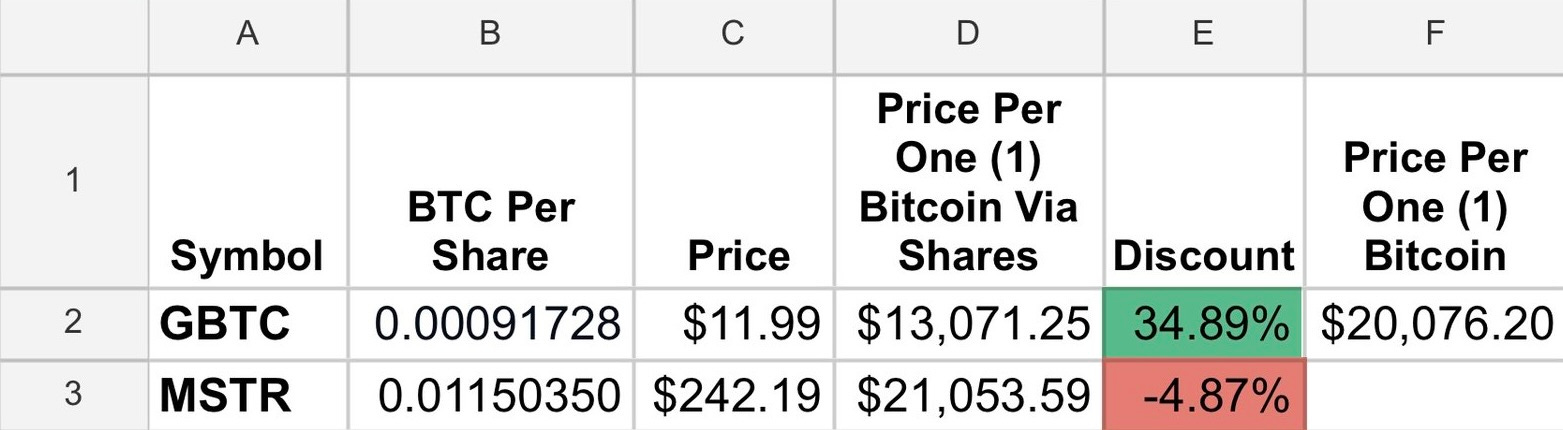

In in this timeframe, probably in 2021 and certainly by 2022, I started to think in bitcoin per share. I’m not sure exactly when. I do know that by 2022, I was posting on X evidence that I was thinking in this way. For instance, on October 5, 2022, I posted the following screenshot of a simple spreadsheet I built comparing the bitcoin per share of the different securities.

The idea was simple. If I could move from GBTC to MSTR, or from MSTR to GBTC, and end up with a larger economic claim on bitcoin, then I had increased my bitcoin-denominated net worth. The trade did not need to be complicated. I just needed a metric to tell me when MSTR or GBTC was undervalued relative to the other.

The Spreadsheet That Changed How I Traded

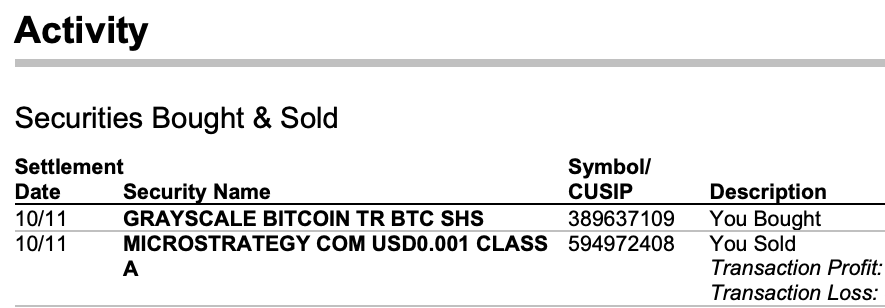

So, for instance, using this spreadsheet to trade between the securities, if I owned MSTR, it would be a good time to sell MSTR and purchase GBTC. Indeed, on October 11, 2022, I did just that. I sold all of my MSTR and bought GBTC with the proceeds. See here:

I would regularly make such trades, and they significantly increased my return.

For instance, in my Roth IRA, from January 1, 2023 to December 31, 2023, I achieved a 466% return. Over the same period BTC returned 155.4%, MSTR returned 337%, and GBTC returned 317.61%.1 Therefore, I beat the best-performing of the three assets, MSTR, by 129 percentage points simply by thinking in bitcoin per share and having the guts to make the trade.2

This was not because the metric was magic. It was because GBTC, MSTR, and bitcoin were temporarily mispriced relative to each other, and the metric helped me see the trade clearly.

Michael Saylor Was Thinking This Way Too

I’m not the only one who was starting to think in bitcoin per share and making decisions accordingly. So was Michael Saylor. I was convinced of this before Saylor ever discussed it.

In fact, on November 30, 2023, on NOSTR, in response to a post by Preston Pysh, I made the following post:

I believe Saylor is laser eye focused on one metric: *sats per share.* He’ll do anything that doesn’t threaten the stack to increase it.

IMO, he’s a brilliant capital allocator.

In the rest of the post, I explained how I had used GBTC, MSTR, and OBTC to increase my own sats, and why I was waiting for the MSTR premium and GBTC discount to converge around the spot ETF launch.

At this point, Michael Saylor hadn’t publicly discussed bitcoin per share. On the August 1, 2023 earnings call, Phong Le, the CEO of MSTR, mentioned it just once when he said, “The primary use of prior ATM proceeds has been to acquire additional bitcoin, increasing bitcoin per share for our shareholders.” Michael Saylor wouldn’t introduce what he called “Bitcoin Yield” until October 2024.

The first time I could find where Michael Saylor discussed bitcoin per share at all was on the eve of the spot bitcoin ETFs being launched, specifically December 19, 2023 in an interview with Bloomberg Crypto. See here:

Note that despite Saylor being a prolific poster on X, especially for a CEO and/or Chairman of the Board of a public company, his earliest tweet mentioning bitcoin per share was the following one on March 20, 2024.

Despite Michael Saylor not discussing his focus on increasing bitcoin per share until December of 2023, it was obvious to many of us who understood both bitcoin and capital allocation that this was what he was focused on. The through-line of Strategy’s capital allocation since then has been the goal of intelligently and responsibly increasing bitcoin per share over the long term.

Why Bitcoin per Share Matters

Total bitcoin owned tells you the size of the stack. Bitcoin per share tells you how much of that stack each share represents.

That distinction matters because a public company has a numerator and a denominator. The numerator is the bitcoin. The denominator is the share count. If Strategy buys more bitcoin but issues too many shares to do it, shareholders may not be better off in bitcoin terms. But if Strategy can issue shares, debt, convertibles, or preferred stock in a way that increases the amount of bitcoin represented by each share, then dilution is not the right word for what happened. Accretion is.

This is the basic formula:

Bitcoin per share = total bitcoin owned / shares outstanding3

This is the corporate version of the same question I was asking in my Roth IRA: how much bitcoin does this thing actually represent?

Over time, the question is whether that number is going up or down.

That is why I do not think about Strategy as merely a company that owns bitcoin. I think of it as a bitcoin capital allocation company. The goal is not simply to own more bitcoin in the aggregate. The goal is to increase the amount of bitcoin represented by each share without taking risks that threaten the stack.

That is also why I think many people misunderstood MSTR for years. They saw stock issuance and thought “dilution.” But stock issuance is not automatically bad. It depends on what the company gets in return. If Strategy sells shares at a premium and uses the proceeds to buy enough bitcoin to increase bitcoin per share, then the issuance can be accretive. If it fails to do that, then the issuance is dilutive in the way people normally fear.

The metric does not make the decision for you. But it tells you what question to ask.

What Bitcoin per Share Does Not Tell You

Bitcoin per share is the metric that measures accretion. It is not the whole analysis.

It does not tell you whether MSTR is cheap. It does not tell you whether the premium to NAV is rational. It does not tell you whether the capital structure is safe. It does not tell you whether a particular financing was wise. It does not tell you whether the preferreds are attractive. It does not tell you whether you should own MSTR instead of bitcoin.

It tells you something narrower but extremely important: whether the actions being taken increase or decrease the amount of bitcoin represented by each share.

That matters because metrics shape behavior. If you measure the wrong thing, you manage toward the wrong thing. If Strategy were only trying to maximize total bitcoin owned, it could issue shares endlessly and buy more bitcoin, even if each share represented less bitcoin over time. That would make the company’s stack larger, but it would not necessarily make each shareholder better off.

Bitcoin per share disciplines the analysis. It forces the investor to ask whether Strategy is growing the bitcoin stack in a way that actually benefits shareholders.

The Point

This is why thinking in bitcoin per share matters.

At the personal level, it helped me compare GBTC, MSTR, OBTC, and bitcoin in a way that made the tradeoffs visible. If a trade increased my bitcoin-denominated net worth, then it was worth considering. If it reduced my bitcoin-denominated net worth, then it needed some other very good reason to justify it.

At the corporate level, the same idea helps explain Strategy. Saylor’s job is not merely to buy bitcoin. His job is to allocate capital in a way that intelligently and responsibly increases bitcoin per share over time.

That is Michael Saylor’s North Star metric.

And once you understand the metric, you can start to understand the machine built to increase it.

Want To Read Further? Start here:

You might think GBTC would track BTC, but keep in mind it was selling at a discount for a large part of 2023. By 2023, we knew the BTC ETFs would likely launch in the beginning of 2024, meaning that GBTC would convert to one and therefore the discount would disappear.

It also helped that there was no tax drag because this was all inside my Roth IRA.

This gets the concept across. The harder question is what share count to use, especially once convertibles, preferreds, and other capital structure details enter the picture. I’ll come back to that in a separate post.